The America First Investment Policy That Got Lost in the Noise

And What it Means for Global Trade Rebalancing and a New Global Economic Order- Article #104

In this 16-minute article, The X Project will answer these questions:

I. Why this article now?

II. What does Section 1 of the “America First Investment Policy” state?

III. What does Section 2 say?

IV. Section 3?

V. Section 4?

VI. Why is This Memo Such a Big Deal?

VII. How does the U.S. Sovereign Wealth Fund Fit Into This Picture?

VIII. Could Greenland and the Panama Canal Therefore Make Sense?

IX. What does The X Project Guy have to say?

X. Why should you care?

Reminder for readers and listeners: nothing The X Project writes or says should be considered investment advice or recommendations to buy or sell securities or investment products. Everything written and said is for informational purposes only, and you should do your own research and due diligence. It would be best to discuss with an investment advisor before making any investments or changes to your investments based on any information provided by The X Project.

I. Why this article now?

The noise is deafening. What noise? Virtually anything and everything being said by almost everyone related to politics and government, and what is going on in the executive branch of our federal government, is just loud noise.

Why is the noise so loud? Because almost everyone is in a highly triggered emotional state, pushing the noise to extreme volume levels. Even for those who withdraw from the front lines of the emotional clashes to the safe and comfortable echo chambers of their social media feeds, the one-sided channel is pumping unintelligible noise in high volumes.

Why is everyone so emotional? We are living through a crisis.

Really? A crisis? What crisis?

Many seem to feel and know it on some level, but very few seem to understand the deep complexity and interrelation of all its different facets. Others are in complete denial and incapable of seeing or believing that there is any crisis at all. Or, they are doing so well with the status quo that they strongly advocate against any changes to anything.

What is this crisis? Well, there is not one. There are many more than I have listed below, and they are all intricately interconnected:

The Federal Debt Crisis

The Federal Budget Crisis

The U. S. Dollar Debasement Crisis

The International Trade Imbalance Crisis

The Net International Investment Position Crisis

The Multi-Polar Geopolitical Realignment Crisis

The National Security Crisis

The Wealth Inequality Crisis

The Affordability and Declining Standard of Living Crisis

The Crisis in Confidence in our Social, Media, and Political Institutions

Again, there are likely many more, but let’s use these ten for this article. Granted, one can argue that any of these is not necessarily a “crisis” per se, but merely a problem that we have been living with for a long time and one that we can likely continue living with for a long time. Sure. Maybe.

When you look at all of these together, and the many more not listed, which all seem to be accelerating and converging, you can see the bigger picture of a significant crisis unfolding. Neil Howe calls it “The Fourth Turning.” Trump calls it “a disaster.” If you accept that we are in a crisis, many things make sense.

Let’s start with a memorandum titled “America First Investment Policy,” issued by President Donald J. Trump on February 21, 2025. This memorandum outlines a strategic approach to foreign investment in the United States.

II. What does Section 1 of the “America First Investment Policy” state?

All four sections are being quoted verbatim, as this memo is essential for everyone to read and understand:

“Section 1. Principles and Objectives. America’s investment policy is critical to our national and economic security. Welcoming foreign investment and strengthening the United States’ world-leading private and public capital markets will be a key part of America’s Golden Age. The United States has the world’s most attractive assets, in technology and across our economy, and we will make it easier for our overseas allies to support United States jobs, United States innovators, and United States economic growth with their capital.

Investment by United States allies and partners can create hundreds of thousands of jobs and significant wealth for the United States. Our Nation is committed to maintaining the strong, open investment environment that benefits our economy and our people, while enhancing our ability to protect the United States from new and evolving threats that can accompany foreign investment.

Investment at all costs is not always in the national interest, however. Certain foreign adversaries, including the People’s Republic of China (PRC), systematically direct and facilitate investment in United States companies and assets to obtain cutting-edge technologies, intellectual property, and leverage in strategic industries. The PRC pursues these strategies in diverse ways, both visible and concealed, and often through partner companies or investment funds in third countries.

Economic security is national security. The PRC does not allow United States companies to take over their critical infrastructure, and the United States should not allow the PRC to take over United States critical infrastructure. PRC-affiliated investors are targeting the crown jewels of United States technology, food supplies, farmland, minerals, natural resources, ports, and shipping terminals.

The PRC is also increasingly exploiting United States capital to develop and modernize its military, intelligence, and other security apparatuses, which poses significant risk to the United States homeland and Armed Forces of the United States around the world. Related actions include the development and deployment of dual-use technologies, weapons of mass destruction, advanced conventional weapons, and malicious cyber‑enabled actions against the United States and its people. Through its national Military-Civil Fusion strategy, the PRC increases the size of its military-industrial complex by compelling civilian Chinese companies and research institutions to support its military and intelligence activities.

Those Chinese companies also raise capital by selling to American investors securities that trade on American and foreign public exchanges, lobbying United States index providers and funds to include these securities in market offerings, and engaging in other acts to ensure access to United States capital and accompanying intangible benefits. In this way, the PRC exploits United States investors to finance and advance the development and modernization of its military.”

III. What does Section 2 say?

“Sec. 2. Policy. (a) It is the policy of the United States to preserve an open investment environment to help ensure that artificial intelligence and other emerging technologies of the future are built, created, and grown right here in the United States. Investment in our economy from our allies and partners, some of whom have tremendous sovereign wealth funds, supports the national interest. My Administration will make the United States the world’s greatest destination for investment dollars, to the benefit of all of us.

(b) Yet for investment in United States businesses involved in critical technology, critical infrastructure, personal data, and other sensitive areas, restrictions on foreign investors’ access to United States assets will ease in proportion to their verifiable distance and independence from the predatory investment and technology-acquisition practices of the PRC and other foreign adversaries or threat actors.

(c) The United States will create an expedited “fast-track” process, based on objective standards, to facilitate greater investment from specified allied and partner sources in United States businesses involved with United States advanced technology and other important areas. This process will allow for increased foreign investment subject to appropriate security provisions, including requirements that the specified foreign investors avoid partnering with United States foreign adversaries.

(d) My Administration will also expedite environmental reviews for any investment over $1 billion in the United States.

(e) The United States will reduce the exploitation of public and private sector capital, technology, and technical knowledge by foreign adversaries such as the PRC. The United States will establish new rules to stop United States companies and investors from investing in industries that advance the PRC’s national Military-Civil Fusion strategy and stop PRC-affiliated persons from buying up critical American businesses and assets, allowing only those investments that serve American interests.

(f) The United States will use all necessary legal instruments, including the Committee on Foreign Investment in the United States (CFIUS), to restrict PRC-affiliated persons from investing in United States technology, critical infrastructure, healthcare, agriculture, energy, raw materials, or other strategic sectors. My Administration will protect United States farmland and real estate near sensitive facilities. It will also seek, including in consultation with the Congress, to strengthen CFIUS authority over “greenfield” investments, to restrict foreign adversary access to United States talent and operations in sensitive technologies (especially artificial intelligence), and to expand the remit of “emerging and foundational” technologies addressable by CFIUS.

(g) To reduce uncertainty for investors, reduce administrative burden, and increase Government efficiency, my Administration will cease the use of overly bureaucratic, complex, and open-ended “mitigation” agreements for United States investments from foreign adversary countries. In general, mitigation agreements should consist of concrete actions that companies can complete within a specific time, rather than perpetual and expensive compliance obligations. More administrative resources, in turn, will be directed toward facilitating investments from key partner countries.

(h) The United States will continue to welcome and encourage passive investments from all foreign persons. These include non-controlling stakes and shares with no voting, board, or other governance rights and that do not confer any managerial influence, substantive decisionmaking, or non-public access to technologies or technical information, products, or services. This will allow our cutting-edge businesses to continue to benefit from foreign investment capital, while ensuring protection of our national security.

(i) The United States will also use all necessary legal instruments to further deter United States persons from investing in the PRC’s military-industrial sector. These may include the imposition of sanctions under the International Emergency Economic Powers Act (IEEPA) through the blocking of assets or through other actions, including actions pursuant to Executive Order 13959 of November 12, 2020 (Addressing the Threat From Securities Investments That Finance Communist Chinese Military Companies), as amended by Executive Order 13974 of January 13, 2021 (Amending Executive Order 13959 — Addressing the Threat From Securities Investments That Finance Communist Chinese Military Companies) and Executive Order 14032 of June 3, 2021 (Addressing the Threat From Securities Investments That Finance Certain Companies of the People’s Republic of China), and actions pursuant to Executive Order 14105 of August 9, 2023 (Addressing United States Investments in Certain National Security Technologies and Products in Countries of Concern). Executive Order 14105 is under review by my Administration, pursuant to the Presidential Memorandum of January 20, 2025 (America First Trade Policy), to examine whether it includes sufficient controls to address national security threats.

(j) This review will build on measures taken under my authority in 2020 and 2021 and consider new or expanded restrictions on United States outbound investment in the PRC in sectors such as semiconductors, artificial intelligence, quantum, biotechnology, hypersonics, aerospace, advanced manufacturing, directed energy, and other areas implicated by the PRC’s national Military-Civil Fusion strategy. Covered sectors should be reviewed and updated regularly, including by the Office of Science and Technology Policy. As part of the review, my Administration will consider applying restrictions on investment types including private equity, venture capital, greenfield investments, corporate expansions, and investments in publicly traded securities, from sources including pension funds, university endowments, and other limited-partner investors. It is past time for American universities to stop supporting foreign adversaries with their investment decisions, much as they should stop granting university access to supporters of terrorism.

(k) To further reduce incentives for United States persons to invest in our foreign adversaries, we will review whether to suspend or terminate the 1984 United States-The People’s Republic of China Income Tax Convention. That tax treaty, along with the PRC’s admission to the World Trade Organization and the related undertaking by the United States to accord unconditional Most Favored Nation treatment to goods and services of the PRC, led to the deindustrialization of the United States and the technological modernization of the PRC military. We will seek to reverse both those trends. United States investors will invest in the future of America, not the future of the PRC.

(l) To protect the savings of United States investors and channel them into American growth and prosperity, my Administration will also:

(i) determine if adequate financial auditing standards are upheld for companies covered by the Holding Foreign Companies Accountable Act;

(ii) review the variable interest entity and subsidiary structures used by foreign-adversary companies to trade on United States exchanges, which limit the ownership rights and protections for United States investors, as well as allegations of fraudulent behavior by these companies; and

(iii) restore the highest fiduciary standards as required by the Employee Retirement Security Act of 1974, seeking to ensure that foreign adversary companies are ineligible for pension plan contributions.”

IV. Section 3?

“Sec. 3. Implementation. The policy set forth in section 2 of this memorandum shall be implemented, to the extent permitted by law and available appropriations, and subject to internal programmatic and budgetary processes, as follows:

(a) With respect to sections 2(a) through 2(k) of this memorandum, the Secretary of the Treasury, in consultation with the Secretary of State, the Secretary of Defense, the Secretary of Commerce, the United States Trade Representative, and the heads of other executive departments and agencies (agencies) as deemed appropriate by the Secretary of the Treasury, and with respect to the authorities of CFIUS in coordination with the members thereof, shall take such actions, including the promulgation of rules and regulations, to support all powers granted to the President by IEEPA, section 721 of the Defense Production Act of 1950, as amended, and other statutes to carry out the purposes of this memorandum.

(b) With respect to section 2(d) of this memorandum, the Administrator of the Environmental Protection Agency, in consultation with the heads of other agencies as appropriate, shall carry out the purposes of this memorandum.

(c) With respect to section 2(l)(i) of this memorandum, the Secretary of the Treasury shall engage as appropriate with the Securities and Exchange Commission and the Public Company Accounting Oversight Board; with respect to section 2(l)(ii) of this memorandum, the Attorney General, in coordination with the Director of the Federal Bureau of Investigation, shall provide a written recommendation on the risk posed to United States investors based on the auditability, corporate oversight, and evidence of criminal or civil fraudulent behavior for all foreign adversary companies currently listed on domestic exchanges; and with respect to section 2(l)(iii) of this memorandum, the Secretary of Labor shall publish updated fiduciary standards under the Employee Retirement Income Security Act of 1974 for investments in public market securities of foreign adversary companies.”

V. Section 4?

“Sec. 4. Definition. For purposes of this memorandum, the term “foreign adversaries” includes the PRC, including the Hong Kong Special Administrative Region and the Macau Special Administrative Region; the Republic of Cuba; the Islamic Republic of Iran; the Democratic People’s Republic of Korea; the Russian Federation; and the regime of Venezuelan politician Nicolás Maduro.

Sec. 5. General Provisions. (a) Nothing in this memorandum shall be construed to impair or otherwise affect:

(i.) the authority granted by law to an executive department or agency, or the head thereof; or

(ii.) the functions of the Director of the Office of Management and Budget relating to budgetary, administrative, or legislative proposals.

(b) This memorandum shall be implemented consistent with applicable law and subject to the availability of appropriations.

(c) This memorandum is not intended to, and does not, create any right or benefit, substantive or procedural, enforceable at law or in equity by any party against the United States, its departments, agencies, or entities, its officers, employees, or agents, or any other person.”

VI. Why is This Memo Such a Big Deal?

The tone and the language are clear: “China, your capital is not welcome here in the U.S.”

What does that mean? Capital controls will be put in place that will not only stop new foreign Chinese capital from being invested in the U.S. but will likely also force (or at least encourage) China to sell some (much? all?) of the U.S. assets they currently own.

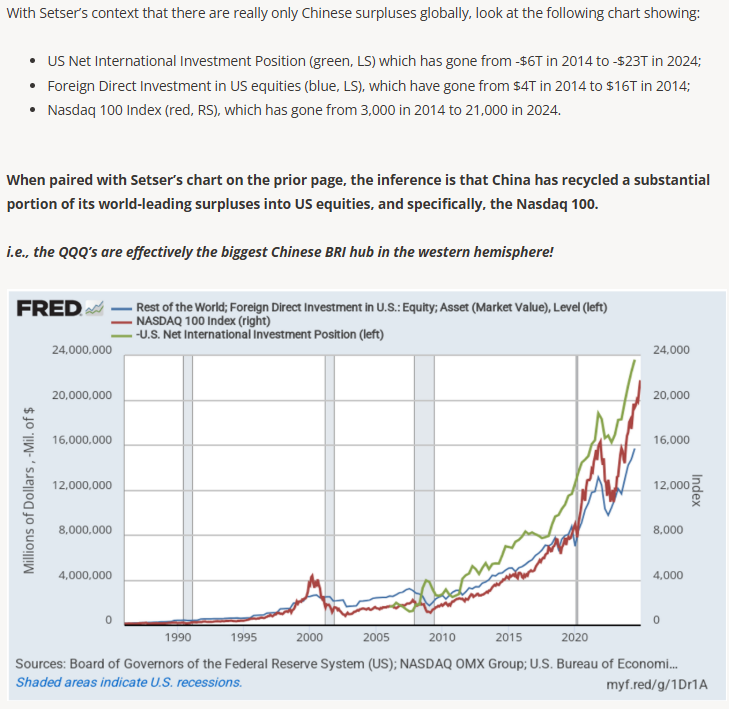

Why would the U.S. want to do this? We are at the losing end of an International Trade Imbalance Crisis. As Brad Setser, an economist and senior fellow at the Council on Foreign Relations, shared on X on February 6th:

China has the biggest surplus, and the U.S. has the biggest deficit. Okay, but aren’t tariffs going to fix that situation, as President Trump has been saying loudly, adding to the noise?

No. The trade account (a.k.a. the current account) is only half of the balance of payments equation, and a given country’s trade account must be balanced by its capital account. As Americans spend more on imported goods and send our dollars abroad, those dollars eventually come back to buy capital - financial assets, real estate, and companies.

Luke Gromen offered this in response to Setser’s comment above in his February 7, 2025 Tree Rings Report:

Note that the U.S. Net International Investment Position is NEGATIVE ~$24 trillion. All of the cheap, disposable consumer goods we have purchased over the last several decades (negative trade balance) have been traded for $24 trillion of our most valuable, prized assets. Which drives which? That is a good question, and many will now argue that the flow of capital drives the flow of trade. Either way, the White House understands the balance of payments equation, and this memo shows that they are attacking the crisis from both sides.

That concludes Section VI. I usually have a paywall after this section so only paying subscribers can read the final four sections. Since it was my birthday yesterday, I want to give all of my subscribers a present and forego the paywall on this article so everyone can read it in its entirety.

All paid subscriptions come with a free 14-day trial; you can cancel anytime. Every month, for just the cost of two cups of coffee, The X Project will deliver three or four articles, helping you know in a couple of hours of your time per month what you need to know about our changing world at the interseXion of commodities, demographics, economics, energy, geopolitics, government debt & deficits, interest rates, markets, and money.

You can also earn free paid subscription months by referring your friends. If your referrals sign up for a FREE subscription, you get one month of free paid subscription for one referral, six months of free paid subscription for three referrals, and twelve months of free paid subscription for five referrals. Please refer your friends!

VII. How does the U.S. Sovereign Wealth Fund Fit Into This Picture?

The Sovereign Wealth Fund (SWF) could be a complete article, and I did learn much about this from Michael McNair’s article. But, I want to provide more of the broader picture so you can hopefully see that there is logic and purpose behind much of the chaos and noise.

The SWF is a countermeasure to foreign reserve accumulation, mirroring policies used by surplus economies like China and Japan. The SWF can actively influence exchange rates, weaken the dollar, and restore trade balance by purchasing foreign assets. This strategic capital deployment enables the U.S. to generate trade surpluses, reversing decades of deficits caused by unrestricted capital inflows.

Other historical economic adjustments have been made, such as the Plaza Accord of 1985, where coordinated currency interventions rebalanced trade among major economies. Unlike prior interventions, however, the SWF provides a unilateral mechanism, allowing the U.S. to act independently of foreign cooperation. This innovative policy tool shifts the focus from traditional monetary mechanisms to direct capital control, enabling the administration to reshape global financial dynamics in favor of U.S. manufacturing competitiveness.

The Trump administration’s broader economic strategy aims to force a global trade restructuring through capital controls, tariffs, and reserve accumulation. The proposed "Mar-a-Lago Accord" that I wrote about in my last article seeks to replicate the success of Bretton Woods and Plaza Accord-era interventions by negotiating currency realignment agreements with surplus economies.

If negotiations fail, the administration can implement unilateral measures, leveraging the SWF, capital controls, and tax policies to pressure foreign governments. These policies would lead to a more equitable global trade framework, where deficits and surpluses self-correct rather than persist as structural distortions. The challenge, however, lies in overcoming resistance from entrenched financial interests and foreign governments reliant on export-driven growth.

VIII. Could Greenland and the Panama Canal Therefore Make Sense?

The mention of acquiring Greenland and controlling the Panama Canal ties into the broader SWF strategy by focusing on key geopolitical assets that influence global trade and capital flows. With its vast natural resources and strategic Arctic position, Greenland offers the potential to enhance U.S. control over critical minerals and energy reserves. Acquiring such assets would strengthen the SWF's ability to accumulate valuable foreign holdings, securing long-term economic leverage.

The Panama Canal, a crucial chokepoint for global shipping, represents another strategic acquisition that aligns with the administration’s objective of influencing global trade routes. By exerting greater control over this infrastructure, the U.S. could reinforce its ability to regulate trade dynamics, ensuring that American economic policies have direct leverage over global supply chains. This aligns with the SWF’s broader function of directing capital flows in a way that maximizes national economic security.

Both Greenland and the Panama Canal fit into the larger strategy of economic rebalancing by providing the U.S. with key assets that counterbalance foreign capital accumulation. These acquisitions would bolster the country’s economic strength and serve as instruments for negotiating more favorable trade terms with surplus nations, ultimately contributing to a more balanced global financial system.

IX. What does The X Project Guy have to say?

One primary reason I launched The X Project and why I am driven to continue reading, listening, watching, learning, and studying the ten topics of The X Project is that I felt, sensed, knew, and understood a lot about how the world worked for the past several decades was going to change. I anticipate and expect these to be core, fundamental changes that will affect everyone and everything. I want to be prepared for and able to take advantage of these changes. Spending time writing these articles helps me organize my thoughts by attempting to educate, inform, and help others understand and prepare accordingly. Over the past fifteen months and 100+ articles I’ve written trying to do just that, I feel the world is proving my original thesis correct.

The answers to why and how the world is changing are constantly evolving, as are the answers to what changes, when, and by whom.

As you know, Luke Gromen is one of my favorite analysts. He recently put together the following, which I want to share because it captures and describes many of the changes we should expect. Please spend a few minutes studying this and thinking about what it means.

First, here is what the world has looked like up until now:

Please re-read it. That picture broadly captures what I have been trying to say is not sustainable and, therefore, will have to change.

X. Why should you care?

Well, guess what is happening? That picture above is changing and essentially reversing. The new picture looks like this:

You don’t have to like Trump (I don’t), and you didn’t have to vote for him (I didn’t). Whether you like it or not, he is our President.

You should filter out the noise and set aside your emotions to understand that he and his team know that we are in crisis and understand the various crises I listed at the beginning of the article. They have a detailed, well-thought-out plan, and they are acting with urgency, purpose, and determination.

What will the result be if they succeed? Here is what Gromen says:

“CAPITAL FLOWS UNDER WHAT TRUMP, BESSENT AND LUTNICK ARE PROPOSING ARE 180-DEGREES OPPOSITE OF THE FLOWS OF THE PAST 40-50 YEARS AND VERY BULLISH FOR US AND GLOBAL GROWTH, THE US INDUSTRIAL BASE, AND GOLD AND BTC. What Trump, Bessent, and Lutnick are advocating will force the world to settle net trade imbalances in a neutral reserve asset…we care not what Bessent says about revaluing gold; if the Trump Administration continues pursuing the policies they appear to be, those policies will likely revalue gold far higher than anyone can imagine.”

However, there will likely be a lot of volatility in markets and asset prices, and probably sooner than later. Especially since, as Gromen says: “The Trump Executive Order appears to have just told the world’s biggest creditor (China) to “take their money and go home.””

Furthermore, with the Federal Government comprising ~25% of our economy, the swinging DOGE axe will likely hit the economy hard.

So… if the economy and asset prices have to take a hit as part of these structural changes, and the new administration knows they need more than four years to re-order the global system, it probably makes sense to tank the market and the economy sooner than later so there is time for a meaningful recovery before the 2028 elections.

Thank you for your free and paid subscriptions. Your support is everything to The X Project and is greatly appreciated. If you agree, please do me the favor of hitting the like button and posting positive comments about my articles - assuming you have positive things to say.

All paid subscriptions come with a free 14-day trial; you can cancel anytime. Every month, for just the cost of two cups of coffee, The X Project will deliver three or four articles, helping you know in a couple of hours of your time per month what you need to know about our changing world at the interseXion of commodities, demographics, economics, energy, geopolitics, government debt & deficits, interest rates, markets, and money.

You can also earn free paid subscription months by referring your friends. If your referrals sign up for a FREE subscription, you get one month of free paid subscription for one referral, six months of free paid subscription for three referrals, and twelve months of free paid subscription for five referrals. Please refer your friends!

Sections IX and X are amazing

wow SWF I love it! Great article. Thanks.