An Introduction to Inflation

What is its relationship to interest rates, government debt/deficits, and fiscal dominance? - Article #9

I. Why is this a topic now?

Last week, on Monday, November 20, The X Project published its first article on Fiscal Dominance. It is a big topic, and it was the first published article that was not a summary of an influential book but an overview of an important subject. It was the first subject covered because the article before it summarized the book This Time is Different: Eight Centuries of Financial Folly. One of the primary conclusions of the book is that there are consequences to too much government debt. Fiscal dominance was not mentioned in the book, but it is a significant consequence of too much government debt and a condition the United States has likely recently started experiencing. The term fiscal dominance recently is becoming more common and a topic of discussion among macroeconomic and investment circles. It is a term that was utterly unknown to The X Project before June of this year. If you still need to read the prior article, you can stop and do that now before continuing to read this article.

The main takeaway from the first fiscal dominance article is that it will likely lead (and probably has already led) to higher inflation. This article will introduce and define the concept of inflation, provide historical and recent context, and explain inflation’s relationship to federal government debt, deficits, and fiscal dominance.

II. What is the definition of inflation?

Inflation will be another significant and recurring topic for The X Project, and there is much to consider about inflation. For starters, let’s first define it.

Inflation is an economic term that refers to the rate at which the general level of prices for goods and services is rising and subsequently, purchasing power is falling. As inflation rises, every unit of currency buys fewer goods and services. It is typically measured as an annual percentage increase.

III. What has inflation done historically and recently?

Inflation is typically measured by the U.S. Bureau of Labor Statistics using the Consumer Price Index (CPI), which is an economic indicator that measures the average change over time in the prices paid by consumers for a basket of goods and services. This basket includes food, housing, clothes, transportation, medical care, and entertainment. There are issues with and criticisms of CPI, and The X Project will explore those at another time.

For now, here is a historical chart of the CPI-U, which measures the spending habits of urban consumers, who represent a significant portion of the total population:

As you can see in the chart and as you are probably well aware, inflation spiked last year and peaked at ~9% in June of 2022, the highest inflation we have experienced since 1981. Over the past year and a half, we have experienced “disinflation,” a declining inflation rate. Note that “deflation” is different and means a negative inflation rate or prices actually falling, and we have only had three episodes of deflation since 1948, as you can see in the chart above.

IV. What causes inflation?

This is potentially a contentious question, and The X Project will explore different theories, arguments, and perspectives in the future. For today’s article, let’s keep it simple. Inflation is or can be caused by several different and various factors, and it is generally accepted that the three most common factors are an increased demand for goods and services, reduced availability of goods or services, and/or an increase in money supply.

When it comes to the most recent spike in inflation, it is generally safe to say that all three factors came into play at different times during the pandemic-induced economic disruption: increased demand for goods during lock-down when services were not available, increased demand for services as lock-downs subsided, a whole variety of different supply-chain issues, etc.

When it comes to the money supply, let’s keep it simple and brief, as this topic will be covered in many future articles by The X Project. A standard and generally accepted measure of the money supply by the Federal Reserve is M2, which includes all of the physical money in circulation, amounts deposited in checking, savings, money market, and other easily accessible and relatively liquid accounts.

Here is a historical chart of M2:

As you can see in the chart, a sharp increase in the M2 money supply coincides with the recent spike in inflation.

V. How do interest rates affect inflation?

We will keep it simple and general for now, as interest rates are another vast topic that The X Project will feature in many future articles. As you are probably aware, the Federal Reserve has aggressively increased the Federal Funds Rate, which is a rate that is set by the Federal Open Market Committee (FOMC) and is the rate at which banks and credit unions lend reserve balances in their accounts at the Federal Reserve to other banks and credit unions overnight on an uncollateralized basis. This rate influences all other interest rates, including savings accounts, money market accounts, mortgages, and loans.

Generally speaking, lowering interest rates usually stimulates the economy by encouraging more borrowing and spending, while increasing interest rates usually dampens the economy by discouraging more borrowing and spending.

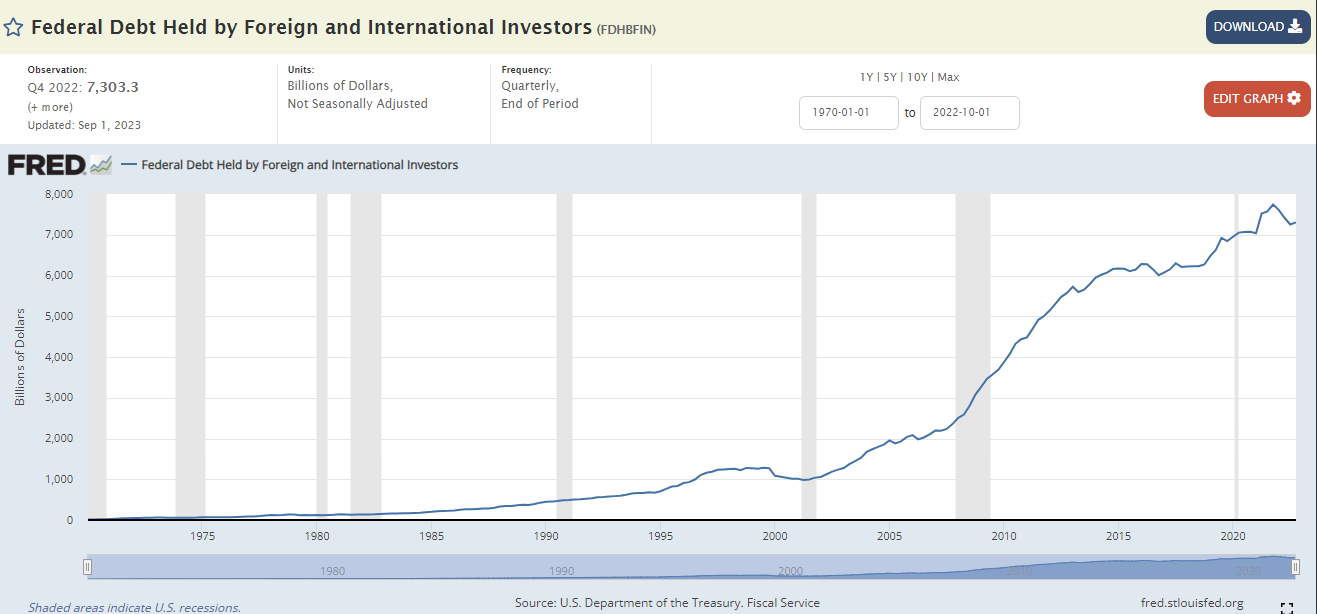

But what happens to interest payments when the total federal debt is more than $32.3 trillion…

… of which $7.3 trillion is held by foreigners…

… and of which $5.5 trillion is held by Federal Reserve Banks…

…leaving $19.5 trillion held by U.S. persons and businesses?

Total annual interest payments increase to $981.3 billion…

…of which $708.2 billion is going to U.S. persons and businesses annually:

This is potentially stimulative for the US economy. Luke Gromen of FFTT has made the argument in his 9/22/23 Tree Rings Report that the only difference between COVID stimulus checks or “stimmys” to everyone and “UST interest payment stimmys is the speed at which the stimmy enters the economy… the latter is like a monetary morphine drip to wealthy asset owners, while the former is like high-grade heroin injected directly into one’s jugular… but either way, the money eventually ends up in the economy over time.”

VI. What is “true interest expense”?

Luke Gromen has long maintained that the “true interest expense” for the US government is not just the direct interest payments on US Treasurys but also Social Security and Medicare payments. Social Security and Medicare payments are effectively “interest” payments on the federal government’s unfunded liabilities

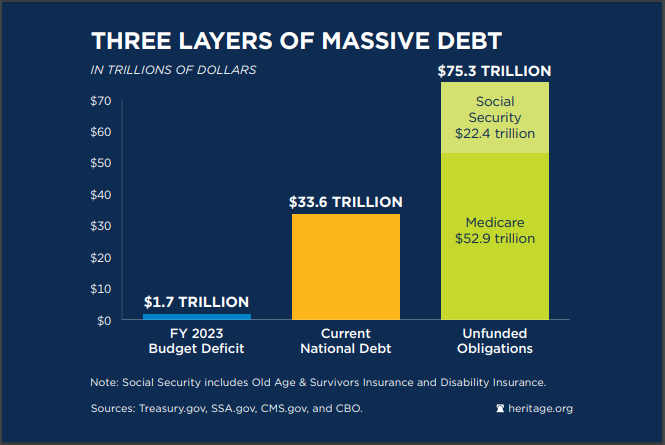

VII. Unfunded liabilities? How much?

The federal government’s unfunded liabilities are for the federal government’s promise to Americans for Social Security and Medicare benefits. The gap between future tax revenues and the cost of those promised benefits exceeds $75 trillion.

VIII. How does “true interest expense” affect the federal budget and deficit?

Let’s first take a look at the official Budget of the U.S. Government - Fiscal Year 2024 (page 142), which was finalized in March of 2023 for the fiscal year starting October 1, 2023:

Hopefully, those reading on small mobile devices can enlarge the image to see the details. The budget summary above groups “mandatory programs” together with a subtotal, and that subtotal plus “net interest” is effectively Luke Gromen’s “true interest expense."

Here is a high-level summary of the outlays (a.k.a. costs or expenditures) for 2024:

Defense = $880 billion or 13.4% of $6.584 trillion in total outlays

Non-defense discretionary programs = $936 billion or 14.2% of total outlays

“True interest expense” = $4.712 trillion or 71.6% of total outlays

Here are the primary points of concern (within the context of this discussion) looking at the budget numbers as they are:

Total receipts (a.k.a. taxes or revenues) in 2024 are expected to be $4.721 trillion, while “true interest expense” is expected to be $4.712 trillion or 99.8% of receipts.

Total receipts for the five years 2024-2028 are expected to be $26.5 trillion, while “true interest expense” is expected to be $26.1 trillion of 98.4% of receipts.

Total receipts for the ten years 2024-2033 are expected to be $60.5 trillion, while “true interest expense” is expected to be $60.3 trillion or 99.6%

And if all of that is not concerning enough, here are the BIGGER problems:

The net interest expense budgeted for 2024 is $796 billion, but the Federal Reserve is reporting that the actual current annualized interest expense as of Q3 of 2023 (7/1/23) is $981.3 billion (see above) or $185.3 billion more than budgeted…

and that annualized amount has been increasing each quarter by an average of $56.9 billion over the past four quarters…

and will likely continue increasing at an accelerating rate (for reasons that will be covered in a future article…

but assuming net interest expense rises at the same rate as the past four quarters, then “true interest expense” is 108.5% of receipts.

The other BIG problem that The X Project will cover in the future is related to tax receipts and why these budgetary estimates for total receipts are overly optimistic…

and you can see a clue to the problem in the budget above where 2023 total receipts are $4.65 trillion, which is down 5% from 2022 receipts of $4.897 trillion…

and until The X Project revisits this topic, you can ponder why receipts fell meaningful from 2022 to 2023 with record-low unemployment and without a recession.

IX. The X Project Guy’s Comments

The article is running long, so I will keep this section to a short multiple-choice quiz:

Q: What do we typically call a company whose revenues don’t cover its interest expense and, therefore, needs to issue more debt to pay interest?

A great stock to sell short (a.k.a. bet on the stock price going lower / likely to $0)A zombie companyAll of the above

Q: What do we typically call a country whose tax receipts don’t cover its interest expense and, therefore, must issue more debt to pay interest?

A country in fiscal dominanceA poorly managed emerging market economy (think Argentina)A debt death spiralAn over-extended empire in declineThe United StatesAll of the above

X. Why should you care?

As you can see from sections V - VIII above, our debt and deficit situation is unsustainable. This debt/deficit “can” has been kicked down the road most of our lives, and the road we’re on leads to a dead-end fast approaching. How will this play out?

No one knows precisely how this will play out regarding the timing and sequence of events, and no one alive today has ever experienced anything like our current situation. But there are historical precedents, and we can (and will) assess possible and probable outcomes.

In the short to medium run, the monetization of the debt is a probable outcome. What does that mean? The X Project will explore that in the future, but in short, it means that the Federal Reserve will (be forced to) “print money” to buy the bonds that the US Treasury will be issuing to fund the government’s deficits and to roll over its debt. Said another way, the Fed will be forced to resume quantitative easing (QE) and implement yield curve control (YCC). This will probably be highly inflationary.

What can you do?

Please help ensure that The X Project can continue its mission.

Please click on the heart icon at the bottom of this article, indicating you like this (and previous) article(s).

If you still need to do so, please subscribe.

Please consider a paid subscription. Until the end of the year, all paid subscriptions come with a free 60-day trial, and you can cancel any time. For the cost of 2 cups of coffee and 1-2 hours of your time per month, The X Project will deliver ten articles per month ($1 per article), helping you know what you need to know about our changing world at the intersection of commodities, debt, deficits, demographics, economics, energy, geopolitics, interest rates, markets, and money.

If you see value in the articles published so far and you see value in the mission of The X Project, please be generous and aggressive in referring friends and promoting The X Project on social media. Click the link to see the rewards as well as the link to use for making referrals

Please let me know how The X Project can better serve you. Please send me recommendations, suggestions, critiques, or feedback at theXprojectGuy@gmail.com.