"Back to the Monetary Future"

Why gold is no longer just a hedge — but a signal that the global monetary order is changing, according to Incrementum's 20th Annual "In Gold We Trust" Report - Article #162

In this 15-minute article, The X Project will answer these questions:

I. Why this article now?

II. Why does the report argue that gold’s bull market is about more than just a rising price?

III. Why does the report say the old monetary order is cracking?

IV. Why does debt sit at the center of the gold story?

V. Why does the report warn that inflation may not be over?

VI. Why does the report say gold is shifting from central-bank accumulation to broader investor participation?

VII. Why does the report argue that the old 60/40 portfolio may be broken?

VIII. What is the report’s big forward-looking conclusion?

IX. Why should you care?

X. What does The X Project Guy have to say?

Reminder: nothing The X Project writes or says should be considered investment advice or recommendations to buy or sell securities or investment products. Everything written and said is for informational purposes only, and you should do your own research and due diligence. It is recommended that you consult an investment advisor before making any investments or changes to your investments, based on information provided by The X Project.

I. Why this article now?

Two and a half weeks ago, Ronald-Peter Stöferle and Mark J. Valek of Incrementum published their 20th annual “In Gold We Trust” report. It is an internationally renowned annual publication that focuses on gold, precious metals, and broader macroeconomic trends. Often dubbed the “gold standard of gold analysis,” it is widely considered a benchmark by investors and central banks globally. [1, 2, 3]

Key details of the report include:

Economic Philosophy: The research and analysis are heavily rooted in the Austrian School of economics, with a focus on sound money, debt cycles, inflation, and government monetary policy. [1, 2, 3, 4]

Scope: While it began in 2007 as a focused precious metals study, it has evolved into a comprehensive 450+-page macroeconomic framework. It now covers inflation, geopolitics, de-dollarization, silver, mining stocks, and digital assets like Bitcoin. [1, 2, 3, 4, 5]

Accessibility: It is published every May and is available globally in multiple languages (English, German, Spanish, Chinese, and Japanese) as a free, compact version or as a highly detailed extended version. [1, 2]

I have covered the two previous reports in these articles that are worth revisiting:

“The New Gold Playbook” - Reviewing Incrementum’s 18th Annual “In Gold We Trust” Report

“The Big Long” - Incrementum's 19th Annual "In Gold We Trust" Report

With gold having retreated to its lowest level since its late-January all-time high, this is a good time to review why owning gold remains a core theme of The X Project.

II. Why does the report argue that gold’s bull market is about more than just a rising price?

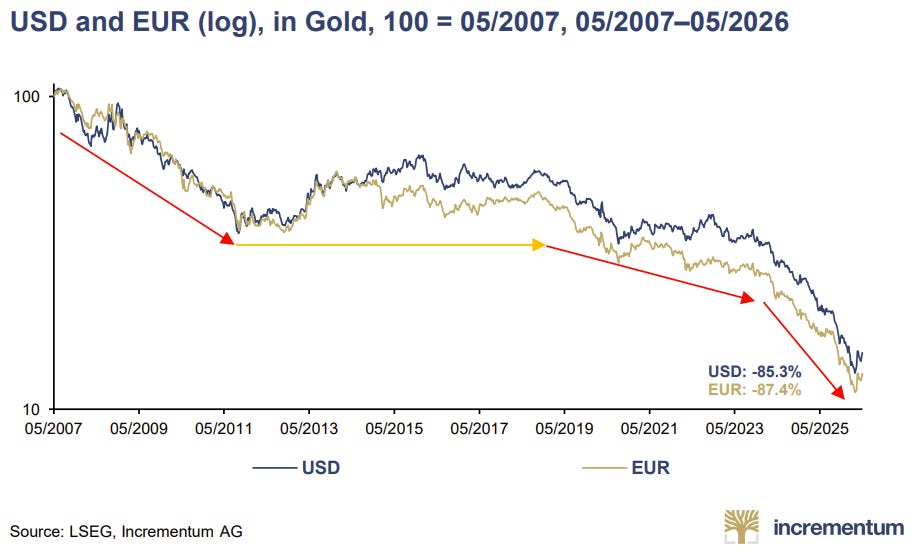

The 2026 In Gold We Trust report makes one big argument: gold’s rise is not simply a commodity trade, a fear trade, or a short-term reaction to crisis. It is the market’s way of pricing a deeper loss of trust in the institutions that sit underneath modern money — governments, central banks, sovereign bonds, and the US dollar-centered global order. The report’s title, “Back to the Monetary Future,” captures the theme: to understand where money is going, we have to return to what money used to be.

The numbers are striking. When the first In Gold We Trust report was published in 2007, gold traded around $670 per ounce. By the 2026 report, gold had increased almost sevenfold, and the report’s long-standing “golden decade” thesis had already been largely confirmed. Gold’s 2025 gain of roughly 65% in US dollars was its strongest annual increase since 1979, and its earlier conservative decade-long target of $4,800 was reached ahead of schedule.

But the authors argue that the more important point is not that gold is “going up.” It is that fiat currencies are losing purchasing power when measured against a monetary asset that cannot be printed. In that framing, gold is not merely an asset with a price; it is a measuring stick. The dollar, euro, yen, pound, and other currencies are being measured against something scarce, neutral, and outside the liabilities of any government.

That is why the report treats gold as a monetary signal. It signals that the post-1945 order, the post-1971 fiat experiment, the post-2008 central-bank rescue regime, and the post-2020 fiscal-monetary fusion are all entering a new stage. Gold is not predicting one specific outcome. It is telling us that the old assumptions about money, debt, inflation, and geopolitical trust are being repriced.

III. Why does the report say the old monetary order is cracking?

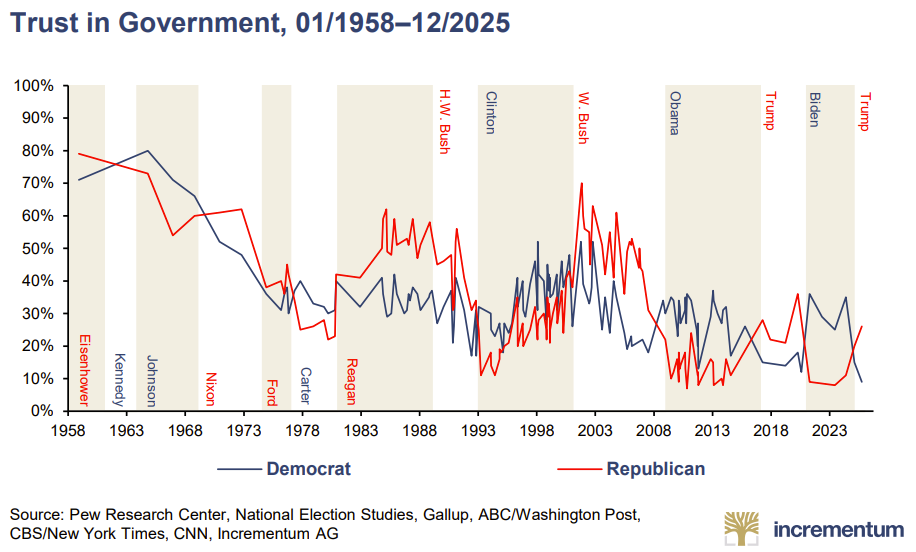

The report argues that the Pax Americana — the political, military, economic, and monetary order that has shaped the world since 1945 — is drawing to a close. This does not mean the dollar disappears overnight or that the US stops mattering. It means the world is moving from one dominant monetary architecture toward a more fragmented, multipolar, and transactional system.

The key driver is trust. The dollar system worked because the world trusted US institutions, US markets, US military protection, US Treasury bonds, and the willingness of surplus countries to recycle savings into dollar assets. But the report argues that sanctions, frozen reserves, fiscal deterioration, energy shocks, war, and geopolitical fragmentation have all weakened that trust. Countries that once viewed dollar reserves as neutral savings instruments increasingly see them as political instruments.

This is where gold returns to the center of the story. Gold is no one’s liability. It does not depend on a central bank, payment system, court system, or political alliance. In a world where countries trust each other less, the appeal of a neutral settlement asset rises. That is why the report sees central-bank gold buying not as random diversification, but as strategic positioning for a new monetary architecture.

The report frames this as a battle between dollarization and de-dollarization, with the US and China building competing financial systems. Stablecoins, dollar liquidity, and US financial infrastructure remain powerful tools for Team USA. But China, Russia, Iran, BRICS-linked initiatives, gold settlement concepts, and Asian financial infrastructure represent the other side of the transition. Gold sits outside both camps — and that neutrality is precisely why it matters.

IV. Why does debt sit at the center of the gold story?

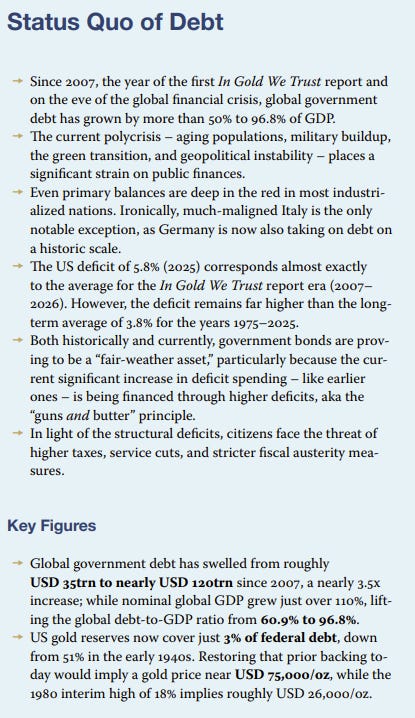

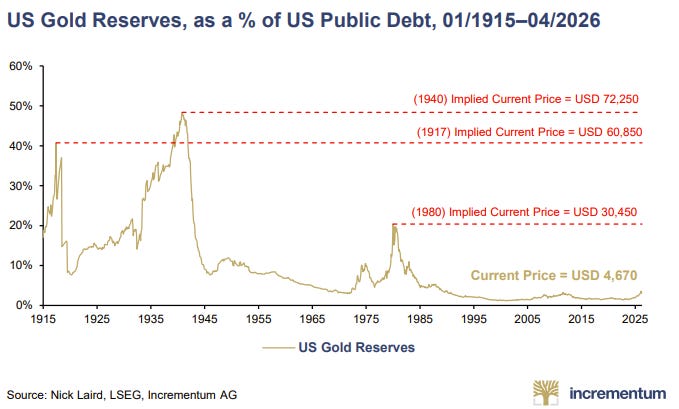

The report’s debt section is blunt: global government debt is climbing inexorably and approaching the 100% of GDP mark. Since the first In Gold We Trust report in 2007, global public debt has risen by more than 50% relative to GDP, while the absolute debt pile has increased far faster than nominal global output. The report’s conclusion is that this is not a temporary post-crisis hangover; it is a structural feature of the new world.

The pressure points are everywhere. Aging populations require more pension and healthcare spending. Geopolitical instability requires more defense spending. Energy transition policies require more public investment. Migration, industrial policy, infrastructure needs, and higher interest costs all add pressure. The result is that governments want “guns and butter” — more defense and more social spending — without admitting the fiscal tradeoffs.

The problem is that the bond market is no longer the automatic escape valve it once was. For four decades, falling interest rates made government debt easier to carry and helped bonds play their classic role in the 60/40 portfolio. But in an inflationary and fiscally stretched world, government bonds become more fragile. The report calls bonds a “fair-weather asset,” useful in stable times but vulnerable when inflation, war, and fiscal stress arrive together.

This is one of the strongest arguments for gold in the report. Gold benefits when government promises are questioned. It benefits when fiscal deficits remain large. It benefits when central banks are forced to choose between inflation control and financial stability. And it benefits when investors realize that a “safe asset” backed by a heavily indebted sovereign may not be as safe in real terms as it appears in nominal terms.

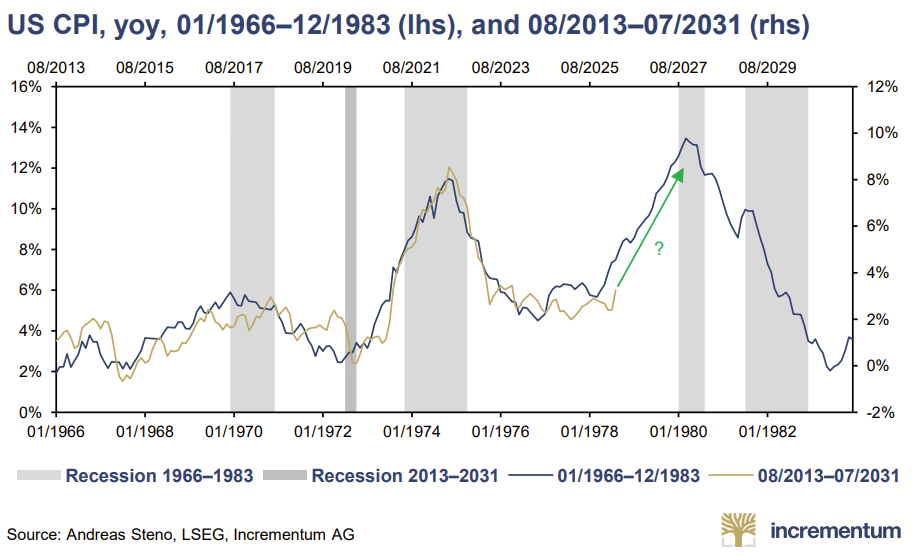

V. Why does the report warn that inflation may not be over?

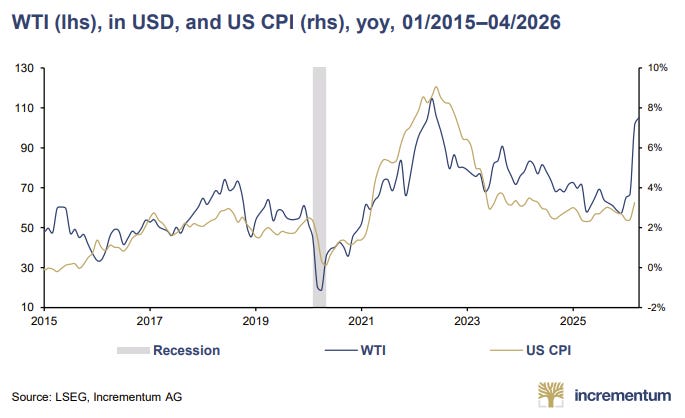

The report argues that the world has entered a period of persistently elevated inflation and higher inflation volatility. Before the Iran war, US inflation had already remained stubbornly above the Federal Reserve’s 2% target for years. The euro area had briefly moved below target, helped by lower energy prices and a stronger euro, but the report presents that relief as fragile.

Then the Iran war changed the inflation landscape. The blockade and disruption around the Strait of Hormuz created a major energy shock. The report notes that Brent crude temporarily moved above $110 per barrel and that a large share of seaborne oil trade and significant LNG volumes were affected. That matters because energy is not just one item in the consumer basket. It is embedded in transportation, food, fertilizer, manufacturing, electricity, chemicals, and global logistics.

The report’s larger point is that inflation is not only about money supply. It is also about social conflict, fiscal choices, supply chains, war, energy security, and political promises that cannot all be honored honestly. If societies cannot agree on who should bear the cost of adjustment, inflation becomes the hidden mechanism that spreads the loss across everyone. In plain English, inflation is how governments avoid telling voters the truth.

This is why gold’s role changes in the report. It is not just a hedge against a single CPI print or a single oil shock. It is a hedge against inflation volatility, policy improvisation, and the growing merger of fiscal and monetary policy. If central banks respond to financial stress with liquidity while governments keep spending, gold benefits from both sides of the policy dilemma.

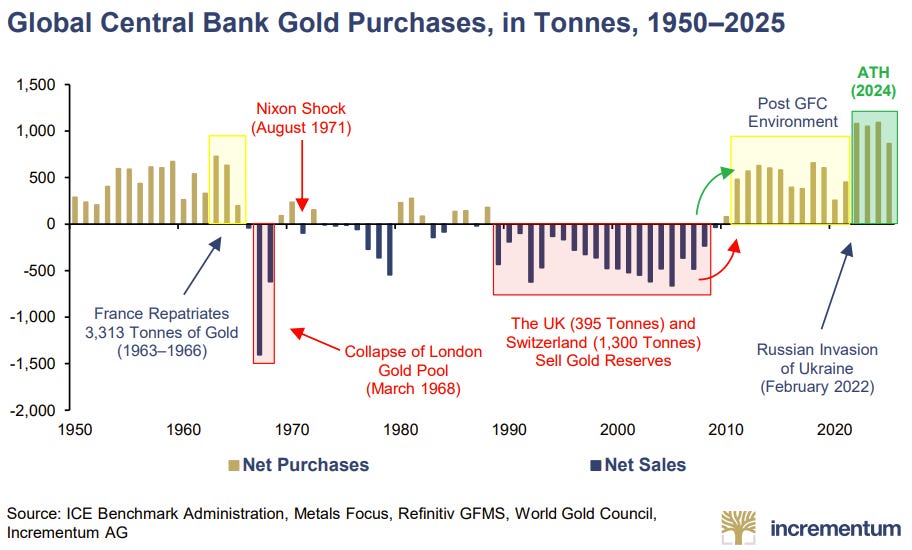

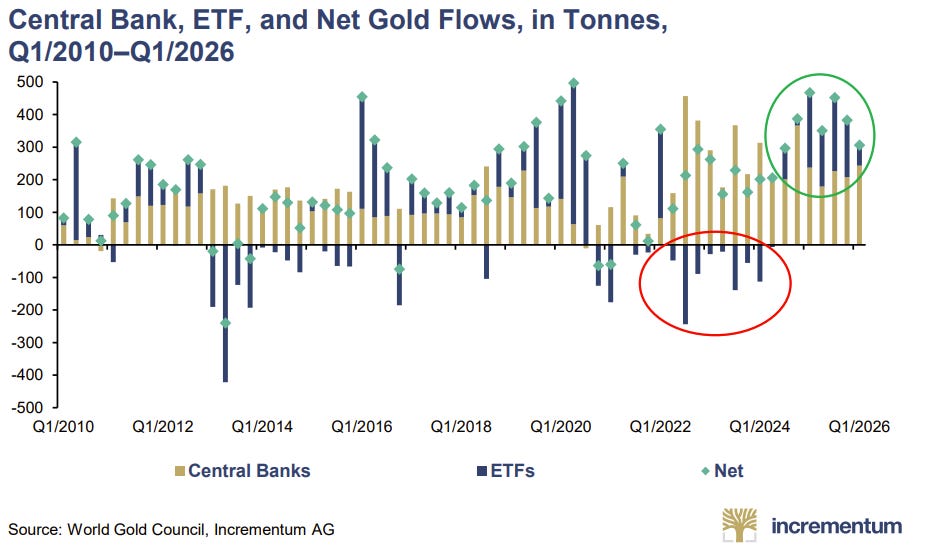

VI. Why does the report say gold is shifting from central-bank accumulation to broader investor participation?

One of the most important takeaways is that the gold market's demand structure is changing. Central banks have been major buyers in recent years, especially since the geopolitical shock of 2022. The report notes that central banks purchased 863 tonnes in 2025 — less than in the peak years of 2022–2024, but still far above pre-Ukraine-war levels.

Central banks are unusual buyers because they are not primarily trading gold for quarterly returns. They buy for strategic reasons: diversification, sanctions insurance, reserve credibility, and monetary optionality. That type of demand is relatively price-insensitive. It helped form the accumulation phase of the bull market.

Now, according to the report, the baton is passing to retail investors, institutional investors, and ETFs. This is the public participation phase of the bull market. Gold is moving from a central-bank-reserve story to a mainstream portfolio story. That is bullish because the pool of potential capital is much larger, but it also makes the market more volatile because investors are more sentiment-driven than central banks.

The March 2026 gold correction illustrates the point. Gold fell sharply during the Iran crisis, not because the thesis failed, but because liquid assets are often sold during stress to meet margin calls and raise cash. The report compares this to 2008 and 2020, when gold sold off during acute liquidity crises before later rallying strongly. In other words, gold can be both the asset people want to own and the asset they are forced to sell during panic.

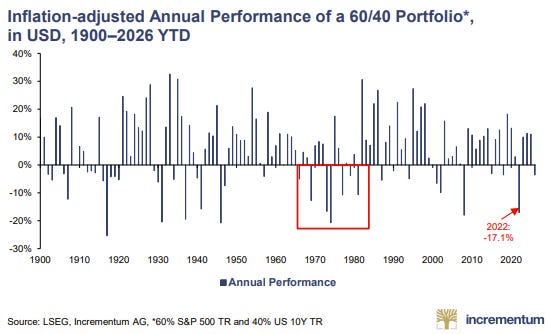

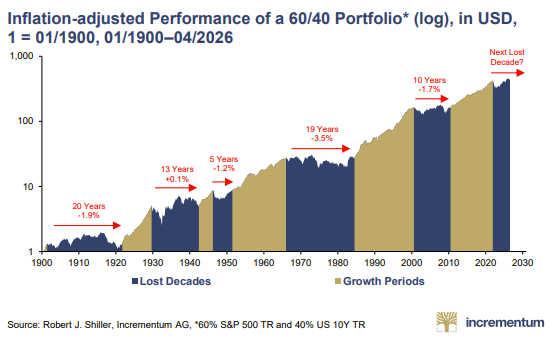

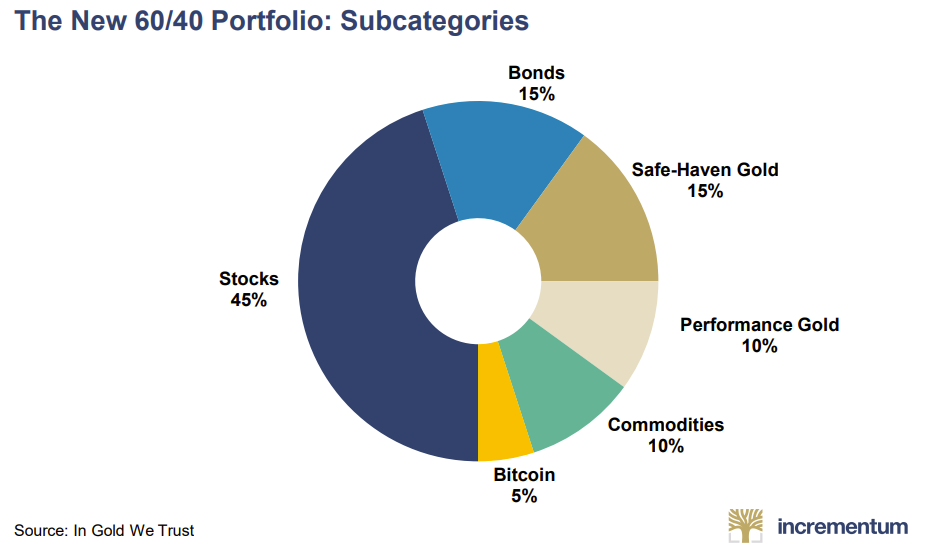

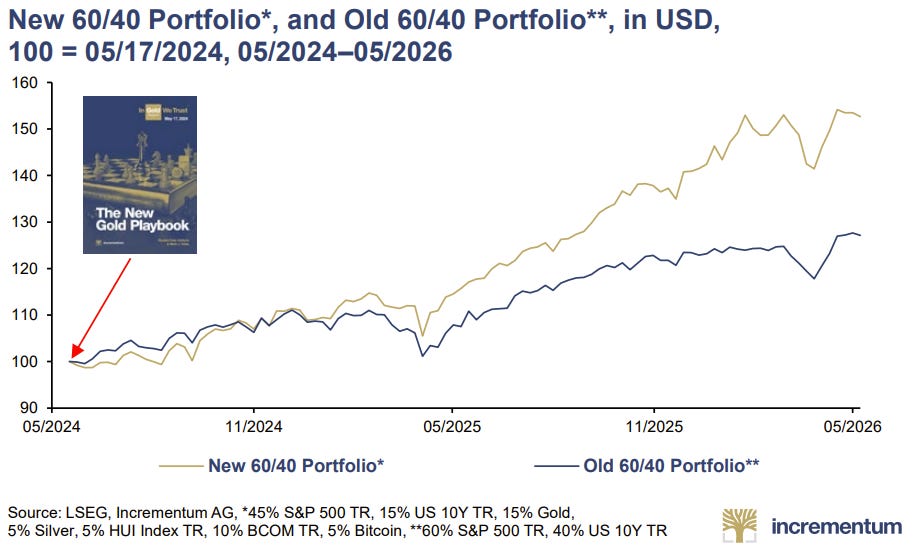

VII. Why does the report argue that the old 60/40 portfolio may be broken?

The report argues that the classic 60/40 portfolio — 60% stocks and 40% bonds — was built for a world that may no longer exist. That world had disinflation, globalization, falling yields, credible central banks, and bonds that usually rallied when stocks fell. In that regime, government bonds acted as portfolio ballast.

But the report says the new regime looks different. Debt is high. Deficits are persistent. Inflation is more volatile. Energy and commodities matter again. Geopolitics is fragmenting supply chains. Governments need to finance rearmament, industrial policy, and the needs of aging populations. In that world, bonds can fall at the same time as stocks because the problem is not a normal growth scare; the problem is inflation, fiscal stress, and rising term premiums.

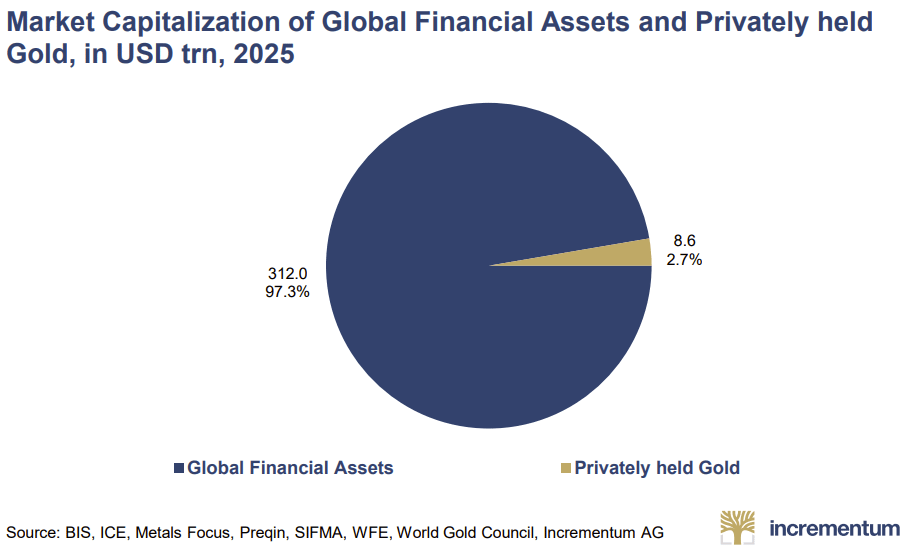

This is where gold’s role expands. The report says gold is no longer merely an insurance policy. It is becoming a return engine in a world where bonds have lost some of their antifragile role. If even a small share of the enormous global bond market reallocates to gold, the impact could be meaningful, as the investable gold market is far smaller than the global fixed-income market.

The report also places gold inside a broader “HALO” framework: heavy assets, low obsolescence. In a world dominated by software, AI, financial engineering, and digital promises, scarce physical assets regain importance. Pipelines, mines, power grids, commodities, energy infrastructure, and gold become harder to replicate and harder to obsolete. Gold is the purest version of that trade: no cash flow, but no default risk, no technological disruption risk, and thousands of years of monetary memory.

VIII. What is the report’s big forward-looking conclusion?

The report’s big conclusion is that gold remonetization is no longer theoretical. It is already underway through central-bank buying, de-dollarization, investor reallocation, possible reserve revaluations, tokenization, Asian gold infrastructure, and discussions around gold-linked settlement systems. The future of money may not be a simple return to the classical gold standard, but the report argues that gold is returning as a key reference point in a fragmented monetary world.

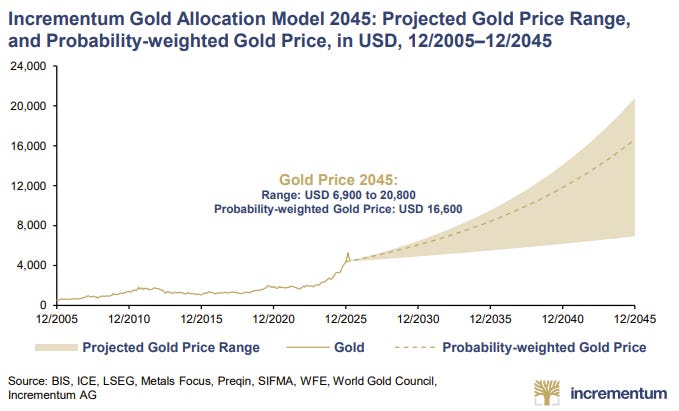

The IGWT Gold Allocation 2045 Model gives this thesis a long-term framework. The model does not claim to predict tomorrow’s gold price. Instead, it asks what happens if a growing share of global liquid assets seeks exposure to a scarce monetary real asset. Depending on the scenario, the report projects a 2045 gold price range from $6,900 to $20,800, with a probability-weighted estimate of $16,600.

The most important point is that gold does not need to become a mania to move much higher. Even modest allocation shifts can matter because global financial assets are enormous while monetizable investment gold is limited. In the report’s framing, the key variable is not mining supply, which changes slowly. The key variable is allocation: how much of the world’s liquid wealth wants protection from debt, inflation, currency fragmentation, and geopolitical mistrust.

For The X Project reader, the message is simple: gold is not just about gold. It is about the condition of the entire monetary system. It is about whether bonds still protect portfolios, whether central banks can control inflation without breaking sovereign finances, whether the dollar system remains unquestioned, and whether hard assets are returning to the center of markets. Gold is the signal. The bigger story is the repricing of trust.

IX. Why should you care?

The reason to care is not that everyone needs to become a “gold bug.” The reason to care is that gold is acting like a dashboard warning light for the entire financial system. When gold rises this strongly across currencies, it is usually telling us something bigger than “investors are nervous.” It is telling us that confidence in paper promises — government debt, central-bank credibility, fiscal discipline, and currency purchasing power — is weakening.

For The X Project reader, this matters because most household wealth is still built around assumptions from the old regime: stocks compound, bonds diversify, inflation settles down, the dollar remains the center of the system, and policymakers muddle through without major consequences. The report challenges those assumptions. It suggests that the next decade may be shaped less by the comfortable math of portfolio theory and more by the hard realities of debt service, energy security, commodity scarcity, war finance, and financial repression - all themes The X Project agrees with and has covered.

That does not mean the right response is panic. It means readers should understand the regime shift. If bonds no longer reliably protect portfolios, if inflation comes in waves rather than one clean cycle, if governments respond to debt pressure by taxing, inflating, regulating, or repressing savers, then the real risk is not volatility. The real risk is quietly losing purchasing power while believing you are being conservative.

Gold matters because it forces a different question: not “what is my return this year?” but “what is my wealth measured against?” In a world where currencies can be printed, bonds can be inflated away, and financial rules can change under pressure, scarce real assets become more than portfolio decorations. They become a way to think clearly about trust, time, and the survival of purchasing power.

X. What does The X Project Guy have to say?

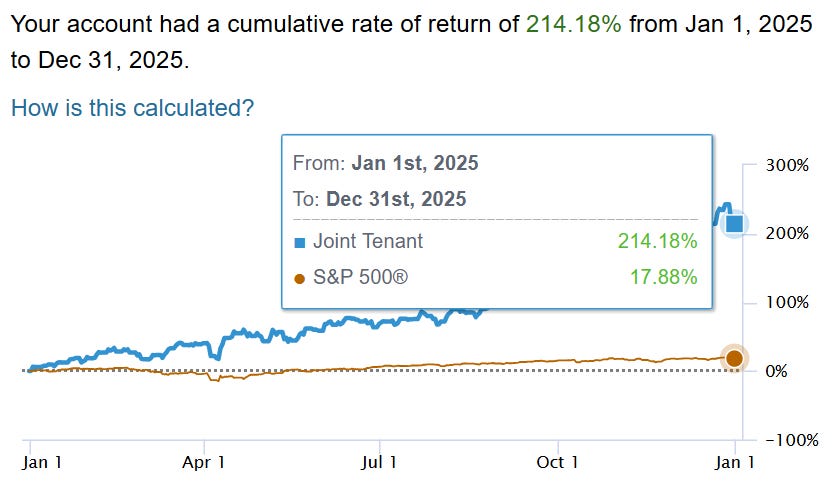

Seventeen articles ago, I put up a paywall and started sharing details of my discretionary investment account, which began in April of 2022, based on The X Project investment themes shared in early 2024 and in most of my articles in 2024 and 2025. Please go back and read them if you haven’t already, as most are still very relevant today.

The X Project investment account (not including my physical bullion) is up 6.7x over the past four years. It was up 214% last year (12x vs. the S&P 500) according to Schwab:

If you are interested in the details of my investment account and how I am managing it, please consider becoming a paid subscriber.

Keep reading with a 7-day free trial

Subscribe to The X Project’s Substack to keep reading this post and get 7 days of free access to the full post archives.