Gold Prices Made New All-Time Highs - Again!

What's Moving Gold, and How High Might Gold Prices Go According to Luke Gromen - Article #102

In this 10-minute article, The X Project will answer these questions:

I. Why this article now?

II. Why Are Gold Prices Surging to New All-Time Highs?

III. How Does U.S. Fiscal Policy Impact Gold Prices?

IV. Is the U.S. Government Preparing to Revalue Gold?

V. What Role Does China Play in the Gold Market?

VI. Are U.S. Elites Preparing for a Gold Revaluation?

VII. What Would $4,000 Gold Mean for the Global Economy?

VIII. Could Gold Become the New Primary Global Reserve Asset?

IX. What does The X Project Guy have to say?

X. Why should you care?

Reminder for readers and listeners: nothing The X Project writes or says should be considered investment advice or recommendations to buy or sell securities or investment products. Everything written and said is for informational purposes only, and you should do your own research and due diligence. It would be best to discuss with an investment advisor before making any investments or changes to your investments based on any information provided by The X Project.

I. Why this article now?

Long-time readers should know Luke Gromen well, as I have highlighted him five times in my previous 101 articles:

Fiscal Dominance - What the heck is it, and why does it matter??

What is the End-Game for the U.S. Debt? And how it might play out, according to Luke Gromen

More Global Economic Shift Viewpoints: A collection of Luke Gromen’s recent non-consensus views

Three things happened this past week. First, gold prices reached new all-time highs:

Second, Scott Bessent said this week, "We’re going to monetize the asset side of the U.S. balance sheet for the American people."

Lastly, I came across this YouTube video on the TFTC channel: USD Devaluation Is Coming, Gold Repricing, Negative Rates, Monetary Reset & Deep Seek - Luke Gromen (54,893 views, January 31, 2025.) That video helped me re-call another video on the same topic from last year on the Market Disruptors YouTube channel: Is the U.S. Gov’t Secretly Rooting for a Gold Price Explosion? | Luke Gromen (43,408 views, August 12, 2024.)

I have been a long-time subscriber of Luke Gromen’s Tree Rings Report, and he has been writing and talking about rising gold prices for many years. The X Project exists for people who do not have the time or the interest in The X Project subjects to consume as much content as I do. The X Project curates, summarizes, distills, and synthesizes knowledge & learning at the interseXion of economics, geopolitics, money, interest rates, debts, deficits, energy, commodities, demographics, & markets - helping you know what you need to know.

Below is a summary of Gromen’s top seven themes, arguments, and considerations for higher gold prices from these interviews and his many Tree Rings reports, plus my additional thoughts and why you should care.

II. Why Are Gold Prices Surging to New All-Time Highs?

Luke Gromen's analysis highlights the key macroeconomic drivers behind gold’s recent price surge. The primary catalyst is the deteriorating U.S. fiscal position, where "true interest expense" has now exceeded 109% of federal receipts, reaching 117% when including Veterans Affairs, according to an analysis of the latest U.S. Treasury Department presentation to the Treasury Borrowing Advisory Committee:

(Please comment below or email TheXprojectGuy@gmail.com if you want me to summarize the Treasury’s latest Quarterly Refunding Documents in an upcoming article).

This unsustainable fiscal trajectory has heightened investor concerns about the stability of the U.S. dollar and the U.S. Treasury market. Historically, when fiscal sustainability is questioned, gold is a refuge against potential devaluation and financial instability.

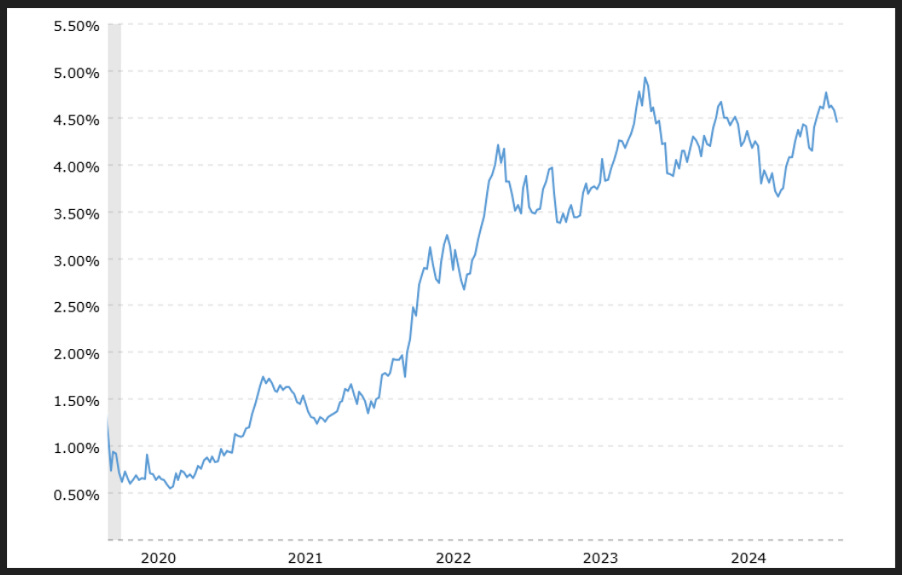

The bond market has already begun pricing in this fiscal stress, with rising yields on U.S. Treasuries, reducing confidence in debt instruments as a haven (below are charts of the yield on the 10-year U.S. Treasury Bond).

Additionally, rising geopolitical tensions, including trade disputes with China and increasing military conflicts, have added a further risk premium to gold. The metal has always been a sought-after asset in times of uncertainty, and with central banks worldwide—including China, Russia, and India—steadily increasing their gold reserves, demand remains strong. The decline of the petrodollar system, the potential for global de-dollarization, and an increasing reliance on alternative reserves all contribute to the continued appreciation of gold.

III. How Does U.S. Fiscal Policy Impact Gold Prices?

The U.S. government’s inability to meaningfully reduce its spending and rising entitlement obligations mirrors the conditions of Weimar Germany’s inflationary spiral, with outlays growing faster than nominal GDP growth and tax receipts.

Treasury Secretary Scott Bessent has retained Janet Yellen’s debt management strategy, prioritizing liquidity rather than structural fiscal reform, despite criticizing it before for not terming US debt over the last two years (Bessent’s Treasury Sticks with Yellen-Era Long-Term Debt Plan, Bloomberg 2/5/25.) Investors recognize that, without meaningful fiscal consolidation, the likely path forward involves a weaker dollar and higher gold prices as a hedge against rising debt monetization.

Furthermore, as deficits expand and debt servicing costs consume a more significant portion of federal receipts, the Federal Reserve will likely be pressured into additional quantitative easing (QE) rounds to absorb the rising supply of Treasuries. Historical data from previous QE cycles shows that such policies often lead to a devaluation of fiat currencies, causing gold to outperform other asset classes. The long-term fiscal outlook suggests a growing reliance on debt monetization, and with real yields turning negative, the case for gold as a store of value becomes even stronger.

IV. Is the U.S. Government Preparing to Revalue Gold?

One of the most striking revelations this past week is Bessent’s statement: "We’re going to monetize the asset side of the U.S. balance sheet for the American people" (Trump orders creation of US sovereign wealth fund, says it could buy TikTok, Reuters 2/3/25). Gromen interprets this as a potential signal that the U.S. may officially revalue its gold reserves to create additional fiscal capacity. If the U.S. Treasury were to mark its official gold holdings to market value—currently marked at $42/oz—this could generate a $745 billion deposit into the Treasury General Account, significantly reducing the need for further debt issuance.

How does this work? Here is an outline of the steps:

Revaluation of Gold Reserves

If Treasury gold were revalued to $4,000 per ounce, its book value would rise to $1.046 trillion. If revalued to $6,000 per ounce, its book value would be $1.569 trillion.

The unrealized gain above the $11 billion at the current mark of $42.22 / ounce can be recognized on the Treasury’s balance sheet.

Accounting for the Gain

The Treasury does not directly spend its gold holdings but accounts for the change in value as a gain.

Historically, when gold was revalued (e.g., under the Gold Reserve Act of 1934), the difference between the old and new value was credited to a Gold Revaluation Account (GRA) at the Federal Reserve.

Transfer to Treasury General Account (TGA)

The Federal Reserve could credit an equivalent amount to the Treasury General Account (TGA) to make the gain liquid.

This would create spendable funds for the U.S. government without requiring new borrowing or taxation.

The Fed would record the increase as a liability to the Treasury, backed by the gold asset at market value.

Historical precedents exist for such actions. In 1934, President Franklin D. Roosevelt revalued gold from $20.67 per ounce to $35 per ounce, effectively devaluing the dollar by 69%. More recently, the Nixon Administration severed the gold standard in 1971 and revalued gold prices to the current mark of $42.22 in 1973.

However, in subsequent years, no administration has since revalued the price of gold on the U.S. Treasury’s balance sheet. If Bessent moves forward with a similar strategy, the effects on global financial markets could be profound, particularly as central banks and institutional investors adjust their portfolios.

V. What Role Does China Play in the Gold Market?

Gromen also highlights the global trade imbalance, particularly China’s record $1 trillion trade surplus. Gromen hypothesizes that Chinese officials argue that their surplus remains high not due to an undervalued yuan but rather because the U.S. dollar is overvalued relative to gold. China has aggressively accumulated gold to balance global trade, with imports exceeding 1,384 metric tons last year. This structural shift could push gold prices significantly higher as China diversifies away from U.S. Treasuries.

China’s gold acquisition strategy aligns with its broader geopolitical ambitions. China reduces its reliance on the U.S. dollar for trade settlement by increasing its gold reserves. This is evident in its recent agreements with key trading partners—including Russia, Saudi Arabia, and Brazil—to settle transactions in local currencies or gold-backed instruments. The Shanghai Gold Exchange has also emerged as a major player in global gold pricing, challenging the dominance of Western exchanges such as COMEX and the LBMA.

VI. Are U.S. Elites Preparing for a Gold Revaluation?

Recent developments in gold swap rates suggest that U.S. financial institutions may be front-running an anticipated rise in gold prices.

According to Gromen, physical demand for gold has been robust, and large quantities of gold have been flowing into the U.S. from foreign vaults. Gromen speculates that this could indicate that well-connected financial institutions anticipate a significant shift in the global monetary system, where gold will play a more prominent role in international trade settlement.

Historically, insider knowledge has played a crucial role in positioning for major economic shifts. The recent accumulation of physical gold by hedge funds, institutional investors, and private wealth funds suggests a growing recognition that a revaluation is imminent. Additionally, U.S. policymakers may prepare to introduce partial gold backing to stabilize the dollar, similar to policies adopted in past monetary crises.

That concludes Section VI. I have hit a new paid subscriber threshold, so you must now be a paid subscriber to view the last four sections:

VII. What Would $4,000 Gold Mean for the Global Economy?

VIII. Could Gold Become the New Primary Global Reserve Asset?

IX. What does The X Project Guy have to say?

X. Why should you care?

If you haven’t done so already, use your free, single-use “unlock” feature to view the rest of this article.

The X Project’s articles always have ten sections. Soon, after a few more articles, the paywall will move up again within the article so that only paid subscribers will see the last five sections, or rather, free subscribers will only see the first Five sections. Please consider a paid subscription.

All paid subscriptions come with a free 14-day trial; you can cancel anytime. Every month, for just the cost of two cups of coffee, The X Project will deliver three or four articles, helping you know in a couple of hours of your time per month what you need to know about our changing world at the interseXion of commodities, demographics, economics, energy, geopolitics, government debt & deficits, interest rates, markets, and money.

You can also earn free paid subscription months by referring your friends. If your referrals sign up for a FREE subscription, you get one month of free paid subscription for one referral, six months of free paid subscription for three referrals, and twelve months of free paid subscription for five referrals. Please refer your friends!