In this 14-minute article, The X Project will answer these questions:

I. Who is Luke Gromen, and Why this article now?

II. Who are the biggest spenders on YOLO?

III. What happens to the spending binge if the stock market crashes or there is a major recession?

IV. What did Charles Gave say in 2018 that was so prescient and insightful?

V. What is the “current account,” and what is it telling us?

VI. Who’s following who?

VII. Will a Petroyuan replace the Petrodollar?

VIII. What is likely at the core of the U.S.-China Stability Pact?

IX. What does The X Project Guy have to say?

X. Why should you care?

Reminder for readers and listeners: nothing The X Project writes or says should be considered investment advice or recommendations to buy or sell securities or investment products. Everything written and said is for informational purposes only, and you should do your own research and due diligence. It would be best to discuss with an investment advisor before making any investments or changes to your investments based on any information provided by The X Project.

I. Who is Luke Gromen, and Why this article now?

Most readers will know Luke Gromen, as I often cite him as one of the most influential macro strategists that The X Project follows. I first introduced Luke in “Fiscal Dominance - What the heck is it, and why does it matter??” I further focused on his work and viewpoints in the following articles:

You can find Luke’s bio in most of these articles, and these are all worth a re-read if you do not remember the main points. Furthermore, they all help paint this picture of a shifting global economy, which is the topic of this article and a follow-up to last week’s article.

II. Who are the biggest spenders on YOLO?

YOLO, as an abbreviation, has been popular for over a decade. More recently, it has become an underappreciated economic force when coupled with demographic reality. Of course, I am talking about the seventy million baby boomers aged 60-78, representing 21% of the U.S. population, approximately half of whom are fully retired. Forbes reported that as of the latter half of last year, approximately 10,000 baby boomers were retiring daily, with four over four million retiring yearly.

According to Luke Gromen, U.S. boomers have $111 trillion in net asset wealth, representing 73% of total U.S. wealth. He points out they are engaging in “the world’s biggest YOLO spending binge.” This is one reason why the U.S. has maintained a growing economy in recent years despite pockets of economic weakness. Of course, the other more significant reason is the U.S. government’s debt-fueled spending binge.

III. What happens to the spending binge if the stock market crashes or there is a major recession?

The boomer spending binge would undoubtedly slow down if there were a stock market crash, but because you do, in fact, only live once and because your lifespan is, in fact, limited, boomers will still likely spend a lot of what they got. And since they are mostly retired, a recession without a stock market crash would not slow them down.

For the U.S. government, it is a different story. Our deficit is currently running at ~7% of GDP. In past recessions (excluding the pandemic), deficit spending rose 6-8% of GDP. Our economy and bond market cannot handle 13-15% of GDP deficits without significant and severe consequences. And therefore, according to Luke Gromen, neither a recession nor a stock market crash will happen because “they” won’t allow it to happen. Let me quote him directly from his August 16 Tree Rings Report:

“3. Even small drops in SPX/ZB (LT UST futures) ratio cannot be tolerated with US “True Interest Expense” this high

Tree Ring: A critical piece of context that seems to have been forgotten by many investors, while many more investors have yet to internalize this reality? US stocks de facto back the UST market. Net Capital Gains + Taxable IRA Distributions are ~200% of the Y/Y growth in US Personal Consumption Expenditures (PCE), which are ~2/3 of US GDP.

If stocks don’t rise enough each year (let alone fall and stay down), US PCE and therefore US GDP mathematically cannot rise. With US debt/GDP at 122% and deficit/GDP at 7%, if GDP does not rise, UST market will go into a debt spiral (receipts down, issuance up, rates up, receipts down, issuance up, wash/rinse/repeat.)

Top 5% of taxpayers pay 63% of Individual income taxes in the US(individual income taxes ~50% of total US receipts.)

A big % of top 5% taxpayer comp comes via stock, option-based, or incentive comp tied to the stock market. In the US, this is taxed as ordinary income, not capital gains or IRA distributions = a statistically significant % of the top 5%’s incomes are expressly tied to the stock market – stocks go up, more options get exercised and sold = receipts up. Stocks fall, fewer options get exercised and sold = receipts down.

Here again: Lower stocks = lower receipts = higher UST issuance = US stocks de facto back the UST market.

While there is no data breaking this out in detail, we can see a glimpse of the significance, as executive stock-based comp sales do not necessarily automatically have tax withheld, so they are called “non-withheld taxes”.

In fiscal 2023, while most economists were surprised by the drop in tax receipts, as you may recall, we were not, because we knew tax receipts would follow stocks.

The screenshot above shows that the majority of the 2023 receipt decline was non-withheld declines. Here again, Lower stocks = lower receipts = higher UST issuance. i.e., US stocks de facto back the UST market.

Chart below = y/y US receipts v. y/y stock performance (equity market cap & SPX.) Since 1995 (when Clinton passed legislation shifting exec comp towards stocks), US receipts fall shortly after stocks fall…and we have seen in recent years that when the economy slows and receipts fall, issuance rises, and unless Yellen shifts it to the front end, the UST market “dysfunctions.” i.e., US stocks de facto back the UST market.

With all that as context, allow us to make our point: SPX de facto backs the US economy and the UST market, so as US government debt has risen, it takes less and less of a sell-off in SPX (in % terms; chart below is log scale) to drive UST market dysfunction and a response from US policymakers (recall we had two extremely weak UST auctions last week, both 10y and 30y):

Our point is this: The prior Tree Ring point highlighting how dire the US fiscal situation is DESPITE rapidly rising tax receipts and at/near full US employment means US policymakers cannot afford to allow SPX/ZB (LT UST futures) ratio to drop much further.

A forecast of a further sustained drop in SPX/ZB (LT USTs) is effectively a forecast of sustained UST market dysfunction, up to and including UST auction failures, followed by a US government and global sovereign debt crisis about which US policymakers do nothing.

This may be intellectually offensive, but we did not allow the system to evolve this way. We continue to keep a sizable UST T-Bill position to weather any (necessarily) brief period that policymakers let the system twist in the wind, but the chart above in the context of the preceding Tree Ring point suggests that policies must be pursued soon that drive SPX back to new highs v. ZB (ditto NDX, Industrials, and gold), as a matter of US national security.

Let’s watch.”

IV. What did Charles Gave say in 2018 that was so prescient and insightful?

Let’s now step back from just looking at the U.S. to look around the world more broadly for more insights on the global economic shifts happening around us.

Charles Gave is the father of Louis-Vincent Gave, the focus of my article last week, and a co-founder of Gavekal. In April 2018, he wrote an article, “The Upcoming Monetary War, With Gold As An Arbiter” in which he said:

“Now, most people tell me that the renminbi cannot become a global currency as it has a closed capital account. The answer to that objection is simple: China has just to offer a conversion in gold to anybody who has too many renminbi. And indeed it is headed in that direction (see The Most Important Change And Its Natural Hedge). In recent years the Chinese have bought all the gold they can lay their hands on, as have the Russians.

So, the real economic struggle between the US and China may not be fought out over trade or technology, but end up as a monetary war. In this regard, watch gold as any significant rise in its price versus the US bond market will be a defeat for Washington; any fall in this ratio should be seen as a victory. In recent years we have been in a stalemate (see chart overleaf). I doubt that this situation will last.”

Note the sentence I emphasized. Now look at Luke Gromen’s chart of the gold to US 30-year government bond ratio:

“Charles: Okay, you are China. You want to de-dollarize the world. So you have to offer a credible alternative to the dollar. You want to de-dollarize not only trade between nations in Asia – if Korea was selling goods to Taiwan, they were settling their accounts, up to two or three years ago, in dollars. And the Chinese are saying, why on earth do we have to use the dollar to settle the account between us? So they are trying to do that.

They are also trying to de-dollarize the oil markets. That has started with Russia. Iran is now selling its oil in Euro. So you have a lot of movement saying that there is something happening also in the oil markets.

So the Chinese want to de-dollarize. But now the problem is that they want also to keep their capital account closed. In simple words, that means that they want to control the money that comes in and out of China. So it’s difficult to tell people you should keep your reserves in renminbi if at the same time you prevent the guys from either investing in China or taking their money abroad. You see what I mean there.

There is a very astute solution that the Chinese have found: It has been to say, guys, look, if you have too many renminbi because you have been selling a lot of oil to China, or whatever, we will settle either in renminbi, you can keep your renminbi in your reserves, fine with us. Or we can give you gold instead of renminbi.

So you have to understand that the gold price is now a big play between the US and China. For the Chinese currency to be credible, a big rise in the price of gold would help them tremendously. Because they have been buying gold like crazy for the last six or seven years. So they have huge inventories of gold. And that is what will ultimately lend a lot of credibility to their currency.

On the other hand, the Americans don’t want that de-dollarization because that’s part of their power. And so what they are trying to do is prevent gold from going up. So, to a certain extent, the price of gold is going to tell you who is going to win in that effort to de-dollarize Asia. If gold goes up, it’s China. If gold goes down, it’s the US.”

V. What is the “current account,” and what is it telling us?

“The current account records a nation's transactions with the rest of the world—specifically its net trade in goods and services, its net earnings on cross-border investments, and its net transfer payments—over a defined period, such as a year or a quarter…

Key Takeaways:

The current account represents a country's imports and exports of goods and services, payments made to foreign investors, and transfers such as foreign aid.

The current account may be positive (a surplus) or negative (a deficit); positive means the country is a net exporter and negative means it is a net importer of goods and services.

A country's current account balance, whether positive or negative, will be equal but opposite to its capital account balance.

The U.S. has a significant deficit in its current account.

U.S. Bureau of Economic Analysis…

A positive current account balance indicates that the nation is a net lender to the rest of the world, while a negative current account balance indicates that it is a net borrower. A current account surplus increases a nation's net foreign assets by the amount of the surplus, while a current account deficit decreases it by the amount of the deficit.”

Now that we know what the current account is and what it means in global macroeconomics, where do we stand? Here is a chart from Luke Gromen that tells you what you need to know:

“The BRICS+ in aggregate run current account surpluses, while the US, EU, Japan, UK etc. run aggregate current account deficits…and within that, it is the US and UK that run the entirety of the current account deficits.”

(If you need a refresher on BRICS, click here. Also, 5-eyes refers to U.S., U.K., Australia, Canada, and New Zealand.)

This chart means that BRICS+ countries are increasing the amount of their net foreign assets, and on that score, they are winning while the U.S. and the U.K. are losing.

VI. Who’s following who?

In recent news, we heard that the U.S. and the U.K. are considering Sovereign Wealth Funds (SWF). This is interesting. According to Luke Gromen:

“Once we understand that a) SWF’s are typically for creditor nations, and; b) the US and UK have historically been the world’s two biggest debtor countries, it begs two questions:

How will the US and UK fund an SWF as debtors?

Why are the US and UK discussing launching SWF’s now?

Answer to question #1: As current account debtor nations, the US and UK will likely fund any SWF’s by borrowing the money…i.e., the US and UK would be shorting the USD to buy USD and GBP assets…i.e., the US and UK SWF’s would be less SWF’s and more “leveraged carry trades.”

Answer to #2: Because they need to, as foreign current account surplus countries are repatriating their capital and/or reinvesting their capital domestically, either due to realpolitik or US sanctions…just as US and UK deficits have begun rising exponentially due to rate hikes and Entitlement program demographics.”

Go back to the chart and quote above.

“Once you realize that, you realize how short-sighted it was for the US and UK to essentially pick a fight with a quorum of the current account surplus countries…and why the US and UK are now talking about SWF’s.

Tactically, the US and UK considering SWF’s appears to be a potential response to what is becoming increasingly acute and obvious – the US and UK have an acute fiscal problem, just as they are starting a fight with a quorum the world’s biggest foreign creditors.

The US and UK need a new source of investment capital to replace these sources of capital, and so they are going to launch SWF’s (which are actually levered carry trade shorts of the USD and GBP more than SWF’s.)

If we take a step back even further and look at the issue strategically, it begs another question:

If the west is winning against the BRICS+ and in particular China and Russia, and if the US and UK’s neoliberal free trade policies of the past 30 years have been so successful, why are the US and UK aggressively shifting their economic model to the economic model of the BRICS+ (industrial policy + SWF)?”

This leads us to Charles Gave and the prior section.

“The chart of gold/LT USTs is conclusively answering the question above: China is winning v. the US.

With the combination of US and UK pursuing SWF’s (and in the case of the US, industrial policy), it appears that the US and UK are pursuing a policy of “If you can’t beat them, join them.” In our view, this is the right strategy for America…but it is secularly inflationary.

Therefore, what US and UK SWF’s + US industrial policy are telling us is that the economic orthodoxy of the past 40 years, of subjugating the US middle and working class AND the US defense industrial base AND the US national security…all to support the bond market via lower inflation…is DEAD.

This is great news for America, for US stock prices, for US working and middle-class wages, for gold, for BTC, and, away from any continued growth scare or (unlikely) recession, terrible for the real value of LT USTs.

Let’s watch.”

VII. Will a Petroyuan replace the Petrodollar?

“9. “Saudi Arabia ‘open’ to Petroyuan, closer China ties, minister says” - 9/9/24

Tree Ring: While we must take the story above with a grain of salt as it is in the South China Morning Post, Reuters reported that meetings were taking place…

…and Xinhua suggested energy trade policy was discussed:

CHINA’S PREMIER LI, IN MEETING WITH SAUDI COMPANY OFFICIALS: ENCOURAGES SAUDI FIRMS TO EXPAND AND STRENGTHEN COOPERATION WITH CHINA IN OIL AND GAS, PETROCHEMICALS, INFRASTRUCTURE, AND TRADE – XINHUA, 9/11/24

A reasonable question would be “Why would Saudi accept the Chinese ‘wampum’ (as Kyle Bass called it) or ‘the red cabbage’ (as Hugh Hendry called it)?”The answer, in our view, is “Chinese goods and gold”…but per the chart below, NOT Chinese gold (which is not allowed to leave China), but rather, western gold shipped to Switzerland, refined and exported out to net settle offshore CNY balances:

Recall that last year the IMF highlighted that China has RMB (CNY) offshore clearing banks in Switzerland (as well as in other major gold trading and refining hubs such as London, Dubai, and Singapore):

Importantly, a chart of gold in CNY since China entered the WTO in late 2001 (below) offers the Saudis and anyone else a persuasive reason to price oil in CNY and net settle in gold:

Gold has risen relentlessly in CNY terms over the past 20 years, on relatively low volatility…the perfect reserve asset, especially post-US sanctions on Russian FX reserves.

When married with Chinese consumer and bank ownership of gold, it sets up a virtuous cycle of “more CNY oil = more CNY oil consumption = more CNY gold buying = higher CNY gold = higher CNY oil consumption, wash/rinse/repeat.” Gold in CNY chart = “the CNY is China’s currency AND China’s problem”, unlike the USD, which is famously “Our currency, but YOUR problem.”

When Russia began reserving large amounts of gold in 2008, the gold/oil ratio was ~8 barrels per oz (8x.) That ratio has steadily trended higher over the past 15 years, and in the aftermath of US sanctions on Russian FX reserves in March 2022, has more than doubled, from 18x to 38x:

It remains poorly-understood that CNY-denominated oil, net settled in gold, should continue to drive the gold/oil ratio ever-higher, as oil markets are some 12-15x bigger than gold markets in annual physical production USD terms; any China/Saudi trade deals would likely only serve to accelerate the rise in the Gold/Oil ratio.

We continue to be significantly overweight gold and gold miners; most investors still do not own gold, and of those that do, relatively few are considering the multi-currency commodity pricing aspect yet. In our view, gold still has a long way to run over time.

Let’s watch.”

VIII. What is likely at the core of the U.S.-China Stability Pact?

The agreement was part of a meeting of the U.S.-China Financial Working Group in Shanghai on Thursday and Friday. Brent Neiman, deputy undersecretary for international finance at the Treasury Department, and Xuan Changneng, deputy PBOC governor, co-lead the working group.

The two sides also exchanged a list of people to contact in the event of financial stress or risk events, the PBOC readout said.

Tree Ring: In staying with the “Read more history and fewer forecasts” theme of the prior point, and noting that “history” says that there are two paths out (currency devaluation and inflation, or austerity, deflation and painfully high real rates), the story above caught our attention…especially when we add in the context of something we wrote about in these pages a number of times earlier this year.

Recall that late last year and earlier this year, US Treasury officials met multiple times with Chinese officials, with the apparent goal of getting China to strengthen the CNY v. USD. Also recall that we have repeatedly highlighted that China IS floating the CNY against gold, and that the CNY was down 30% v. gold from mid-2023 to January 1, 2024, and that the CNY is now down 55% v. gold since mid-2023 (see chart above).

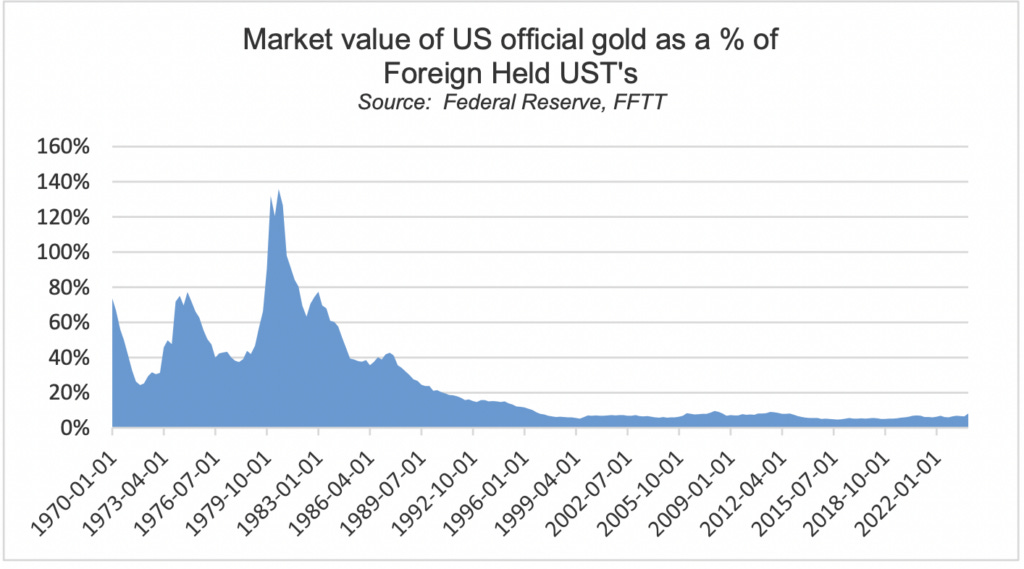

Recall further that we suggested that in our opinion, China likely told Treasury Secretary Yellen and her colleagues that “If you want the USD to fall v. CNY, then you need to let the USD price of gold rise, a lot”, because the USD is wildly overvalued v. gold – the long-term average of the market value of US official gold as a % of foreign-held USTs is 40%. Today, at $2,500, that ratio is just 8%.

i.e., Gold would have to rise 5x just to get back to the long-term average of the ratio charted at right.

With China devaluing the CNY v. gold, if the US wants the USD to fall v. CNY, then the US is going to need to let the USD fall significantly v. gold.

Interestingly, shortly after the Yellen Treasury began meeting with China about strengthening the CNY v. the USD and we speculated that the Chinese told Yellen to “let the USD price of gold rise”, the USD price of gold began rising (and we heard credible rumblings Treasury had begun bidding gold higher via proxies.) In recent weeks, around the US/China meeting above, gold broke out to new all-time highs…

…which has suddenly begun strengthening CNY v. USD a bit:

…while the breakout in USD gold has coincided with a drop in the broader DXY index…

…with the weaker DXY helping to contain 10y UST yields (candle chart):

It is not often we see a major asset class that needs to rise 5x just to get back to LT historical averages, let alone one as under-owned in the west as physical gold…but here we are.

We have not just “History” in our favor (the US and the west needs a much weaker USD), but we have means, motive, and now, with this US/China meeting, potential opportunity.

We have detailed the ways that gold is re-entering the system as a neutral reserve asset to net settle local currency commodity-related trade imbalances, particularly among the BRICS; we have also described how the US could use gold in binary fashion to recapitalize its sovereign balance shhet; now we are flagging the possibility that gold is being used as the pivot to move currencies to “where they are needed”…

…just as former US Treasury official and World Bank President Robert Zoellick advocated back in 2010:

Robert Zoellick, a former US Treasury official, calls for a system that “is likely to need to involve the dollar, the euro, the yen, the pound and a renminbi that moves towards internationalization and then an open capital account”.

He adds: “The system should also consider employing gold as an international reference point of market expectations about inflation, deflation and future currency values.”

Let’s watch.”

IX. What does The X Project Guy have to say?

This is a delicate and intricate tapestry being woven, and hopefully, you can see the emerging broader patterns. Since this article is much longer than most, I will keep my comments short.

Buy gold and keep buying gold.

X. Why should you care?

Because the purchasing power of our currency is likely to erode at an accelerating pace.